Understanding LISA interest rates: a comprehensive guide

Understanding LISA interest rates is crucial for individuals looking to make informed d...

How much does it cost to invest?

It may come as a surprise, but you have to pay for investments, whether you use an adviser or not.That’s because the people looking after your money need to be paid for the work they do.

There’s no such thing as a free lunch!

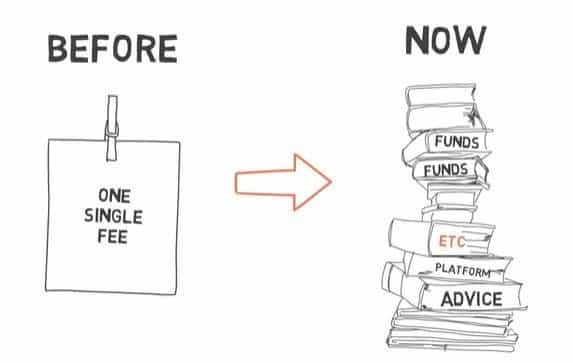

Fees are generally charged as a percentage of the money you’ve invested and since 2013, when the government introduced new rules, each bit of the service has to be separately paid for.

Previously, fees were all bundled up into one charge. But now, each bit charges you separately.

There’s the custody and administration fee, the wrapper fee, the funds, and if you’re using an adviser, there’s also an adviser fee.

As a rough guide, you’re probably going to pay around 1.6 percent of your investments per year.

In real money terms, if you have an ISA of £15,000, that means you will be paying about £240 per year.

In particular, platform fees can vary enormously, so it pays to choose the right platform for you.

Some platforms charge a flat rate and some charge as a percentage.

On a typical £15,000 ISA investment, the fee can range from £12.50 to £400.

So it definitely pays to shop around!

Of course, fees are not the only factor. You may prefer to have a platform with lots of bells and whistles, such as lots of tools and research.

A platform with all the bells and whistles will obviously cost more than one that is offering bog-standard custody.

Product wrappers also have a charge. Most platforms won’t charge for an ISA, much like most banks not charging for a current account. But in general, SIPPs and other life insurance type products will have a charge of some kind.

Again, the cost of the SIPP can vary from platform to platform. Some will offer them their own SIPP and some also give access to third-party SIPP providers.

The advice fee. If you choose to use an adviser, he would discuss his fee with you, whether it’s a one-off fee or an ongoing annual fee.

The fee could be a flat rate or it could be a percentage of your assets.

The adviser may charge for his advice and the time spent reviewing your case even if his advice is ultimately to change nothing, or to do nothing for the time being.

Which is absolutely fine, because his job is to review and monitor your financial affairs and only make changes if necessary.

Doing nothing generally means that you’re on the right track!

Fund fees.

The fund manager will also charge an annual management charge, this is sometimes called an ongoing charge figure.

Fees can range from as little as 0.05% for a passive index tracker to more than 1.5% for an exotic, successful and performing equity fund.

Neither is wrong!

It really just depends on what you want from your investments, the risk you want to take and how long you want to invest for.

Passive funds simply track the index or indices whereas in actively managed funds, fund managers use their research, skills and knowledge to try to beat the index and deliver superior returns.

So let’s look at the impact of fees.

Higher charges can eat into your returns over the long run. You should aim for positive returns net of all fees, if the exotic equity fund we mentioned earlier, is still generating a good return, after the 1.5% management fee and the 0.35% platform fees have been taken off, that’s all well and good!

But if not. You might want to review your options…

Let’s assume that you invest £15,000 in an ISA. And that you’re aiming for a steady return of 4%. If charges amount to 2% a year. After 20 years, you’ll have an investment of £22,375. Which isn’t too bad…

But, if charges were just 0.7% a year for example. Your investment would have grown to £29,962.

That’s around £7,000 difference! So that’s why it pays to understand fees.

CLOSE

Exciting news! We’ve revamped our brand and moved to a box-fresh consumer site — Compare+Invest has replaced CompareThePlatform (make sure you update your bookmarks).

Are you an adviser?

Don’t worry, we’ll still provide you with the tools and content you need, but we’re doing it on an adviser-dedicated site with a host of additional content and features.